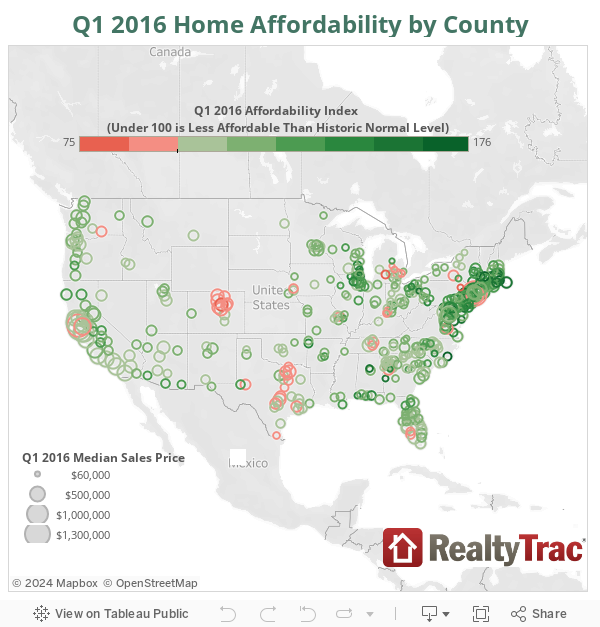

Wage growth has largely failed to keep up with rising home prices in many major metro areas across the nation, according to RealtyTrac’s 2016 Home Affordability Index. The real estate data firm’s latest study shows 9 percent of U.S. counties are less affordable than their historical normal levels, up from 2 percent one year ago.

“We could kind of see this coming,” said Daren Blomquist, senior vice president at RealtyTrac. “It really is about the absence of wage growth to me. But how the market has taken off– [it] has really not been supported by a recovery in the broader economy, or at least a robust recovery. That’s why you see 61 percent of the counties we looked at where home price growth outpaced wage growth.”

[Tweet “@RealtyTrac: The average earner dedicates 30.2%/month of income toward the #mortgage”]

Nationally, the average wage earner needs to dedicate 30.2 percent of income per month toward the mortgage — both property taxes and insurance included — on a median-priced home of $199,000. In the first quarter of 2015, the ratio of income-to-mortgage-per-month was much lower at 26.4 percent.

Home price is outpacing wage growth in 61 percent of markets, while wage growth is outpacing home price in 39 percent of markets.

New York and San Francisco: Home prices outperform wages

The major contenders for unaffordability include New York City and San Francisco, which also top the list for the five most-populated county housing markets that are less affordable than years past, including New York’s Kings County (Brooklyn) and New York County (Manhattan).

“In some of these markets, home price growth is somewhat inflated by foreign buyers coming in with cash who are willing pay more in New York or Miami than a local buyer, who might not be wiling to, which is pushing up prices,” Blomquist said. “But, really what’s causing this affordability piece, is wages have not kept up.”

In Kings County, home prices have risen 42 percent since the market bottomed out in the fourth quarter of 2011. However, wages have only risen 3 percent — representing a massive disconnect between the real estate market and income increases.

In Marin County, located just north of San Francisco, home prices grew 52 percent, whereas wages have been flat. Blomquist emphasizes how this economic detachment illustrates that wages are the outlier, and in Marin County, even over the long term, we can see home prices outpacing wage growth.

“Places like Manhattan and San Francisco County have always been unaffordable. If you’re making the average wage there, you’re spending a lot to buy,” he said. “It’s one thing to say they are unaffordable compared to the rest of the country, but to say they are unaffordable compared to themselves says we are starting to surpass that threshold.”

Chicago, Miami and Baltimore: Affordable, despite little movement in wages

Chicago, located in Cook County, has only seen 3 percent wage growth year-over-year, but the city is within the top 20 county housing markets for most affordable compared to historical norms. Moreover, Cook County and Chicago are in the five most-populated housing markets that are more affordable than their historical norms.

Similarly, Baltimore is a market benefitting from more affordability now in the first quarter of 2016 than ever before, but it’s not wage growth that’s keeping buyers from overspending. Since bottoming out, home prices have decreased 3 percent in Baltimore County.

“The level of demand, particularly from outside buyers who aren’t constrained by wages, isn’t in places like Baltimore and Chicago as much, so prices have stayed more in line with what people can actually afford,” Blomquist explained.

Miami is also a market more affordable than historic levels, with average buyers allocating 36.7 percent of wages toward mortgage payments. The normal rate in Miami is 40.7 percent of wage spent on mortgages.

LA and Houston: more affordable based on size

While Los Angeles and affordable aren’t exactly synonymous — in fact, according to Blomquist, the average earner must spend 67 percent of income to buy a median-priced home — L.A. is still within the range of past portions of income spent on housing.

“Unlike San Francisco and Manhattan, L.A. is still within the safe range of what people are willing to pay over the past 10 years. It’s not LA compared to other cities, but to itself,” Blomquist said. “Houston is similar.”

In Harris County, wage growth is flat, but the percent of income spent on mortgage is lower than the national average at 22 percent.

More professionals continue to infiltrate cities, especially on the coasts, and push home prices up. While jobs might be soaring, income levels aren’t helping offset the costs in many major cities.

“We’re seeing more jobs, but not a lot of growth in average wages,” Blomquist said.