This post has been republished with permission.

The MLS segment of the real estate industry will achieve a major milestone in 2019. The number of multiple listing services in the United States will drop below 600.

Understanding the MLS landscape is a complex task. This report visualizes data in the MLS space to give big-picture context on the relationships between consumers, real estate agents, brokerages, listings and MLSs.

What is an MLS in 2019?

An MLS is more than a database of listings and the software that is used to access it. It is an organization with staff, agreements with multiple vendors for services related to listings, showings, additional data, contract forms and more.

The MLS is a collective of brokers that establishes and enforces rules for cooperation and compensation for sales. This is the foundation on top of which a technology platform exists.

Size of MLSs in the U.S. by agent count and listing count

Why does this data matter?

Each individual MLS organization has its own expenses for managing labor resources, relationships with vendors and brokers, and rules/permissioning for access to its services and listing data.

A relatively large number of MLS organizations in one geographic area can correlate to a high overhead cost that is passed on to the MLS’s customers: brokers and agents. Duplication of services and siloed data result in financial and operational inefficiencies for these customers.

Why is this analysis important now?

Leaders in the real estate industry have been asking for broad insights into the state of MLS. When they analyze the global atmosphere for collaboration, they need good data: overlapping market visuals, and comparative regional and marketplace variables. Visuals tell a memorable story of the underlying data.

The big picture: Where MLS is trending

This report illustrates the state of MLS, to assist the real estate industry in understanding the space more fully and guide its evolution:

- How the number of MLSs is shrinking over time

- Why this trend is gaining momentum in MLSs and associations

- State-by-state figures on the number of MLSs per agent, per listing and per population

- Concentration of agents in different populations and the influence of home prices by state and listing-to-agent ratios in MLSs

- Regional variances in MLS attributes that point to historical association and MLS relationships’ effects on neighboring markets

- Conclusions: Informed analysis and strategy needed

MLSs can range from organizations with over 100,000 working real estate agents to small cooperatives with just a few dozen members. Some markets are covered by multiple overlapping local MLSs, while others have a single MLS that covers a broad geography or even multiple states.

The volume of listings an MLS makes available to members and subscribers — brokers and agents — is a major factor in the relative value these customers place on each MLS organization.

Where we are today: 600 MLSs in 2019

MLS brokerage cooperatives were originally created by brokers, usually within Realtor associations, to set rules for sharing each others’ listings and creating certainty that they’d be compensated by one another for sales.

Thousands of MLSs existed at one point, but the numbers have shrunk significantly in recent years. Brokers have encouraged some MLSs to consolidate, to improve cost and staffing efficiencies, as well as to access greater geographic coverage with fewer constraints.

Why is the number of MLSs shrinking?

Trends: Number of MLSs organizations and Realtor associations (projections through 2019)

Trends: Number of Realtor members (projections through 2019)

While the agent population ebbs and flows with the market, associations and MLSs have been continually shrinking in unique organization counts. This trend comes from both organic drivers and organized industry action.

Some associations and MLSs have merged organizations to better serve brokers’ increasing needs for technology and more nimble support systems.

Others have folded themselves into larger organizations or joint ventures as NAR’s Core Standards requirements (begun in 2014) set a minimum standard of service that they were not able to achieve on their own. NAR provides consolidation resources to help with the process.

MLS consolidation can mean:

- Organizations being acquired

- Organizations merging

- Data and resource sharing

- Technology and legal partnerships to streamline data access, and more

Why is this trend gaining momentum?

Cumulative number of agents served by number of MLS organizations

As real estate went online in the late 1990s, MLSs went from in-office listing sharing tools to an externally available business function. MLS organizations had to evolve technologically.

At the same time, brokers realized efficiencies with technology that allowed them to serve broader geographies and more agents. They needed MLSs that could grow dynamically with them.

The transition over 20-plus years left some MLS organizations — often smaller in size — struggling to provide modern technology and service levels due to lack of resources and staffing. Many merged their organizations into larger regional MLSs.

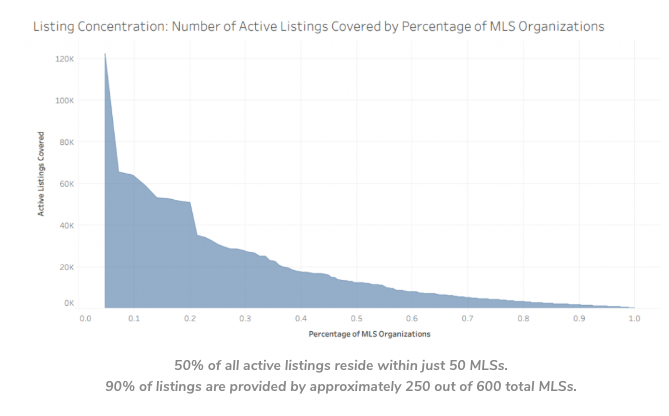

Number of active listings covered by cumulative percentage of MLS organizations

The vast majority of agents and listings reside within a small fraction of the MLS organizations in the United States; 150 of the 600 MLSs in existence today have 90 percent of the agent population within their ranks.

Half of the agents are in just 20 MLSs.

Nine out of 10 listings can be found in fewer than half of all MLSs: 250 organizations. The long tail of MLS organizations is highly pronounced. Note that hundreds of MLSs don’t appear on the cumulative agent concentration graph — their agent count doesn’t register statistically.

Information about MLSs is often siloed in local MLSs that don’t share data with their neighbors. The National Association of Realtors’ RPR (Realtors Property Resource) is one of the few unifying sources that covers the vast majority of MLS marketplace data and is the basis for this report. Where RPR’s contracts don’t cover certain MLSs, data from other sources has been added.

The regional picture: MLSs across the United States

The number and size of MLS organizations varies widely across the country’s different regions:

MLSs by agent count and listing count in the Northwest United States

MLSs by agent count and listing count in the North and Central United States

MLSs by agent count and listing count in the Northeast United States

MLSs by agent count and listing count in the Southeast United States

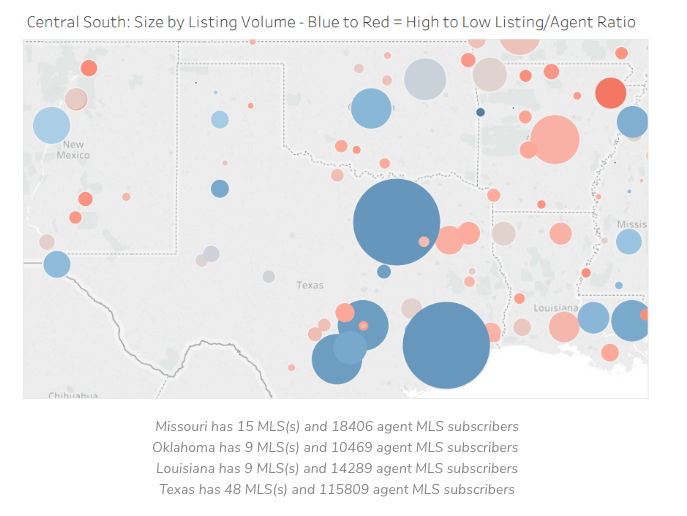

MLSs by agent count and listing count in the Central Southern United States

MLSs by agent count and listing count in the Southwest United States

MLSs by agent count and listing count in the Southwest United States

MLSs by agent count and listing count in Hawaii

State by state: Understanding the MLS landscape

State-by-state data creates a picture of where the number of MLS organizations is relatively high in comparison to the local listing, agent and population numbers. These are indicators as to where there might be more costly organizational overhead and barriers to accessing markets and data.

States’ number of MLS organizations in relationship to total agent MLS subscribers

States’ number of MLS organizations in relationship to total active listing counts

States’ number of MLS organizations in relationship to total population

States’ effects on the MLS landscape

State data provides a picture of some regional similarities. The number of MLSs, as compared to agent headcount, seems to be highest in clustered areas. The results are similar for MLSs per active listing and per general population. The locations with the highest organizational MLS overhead look much like their contiguous markets.

When looking at regional markers, governing bodies can analyze the variance in organizational structure and listing volume delivery relative to the rest of the country.

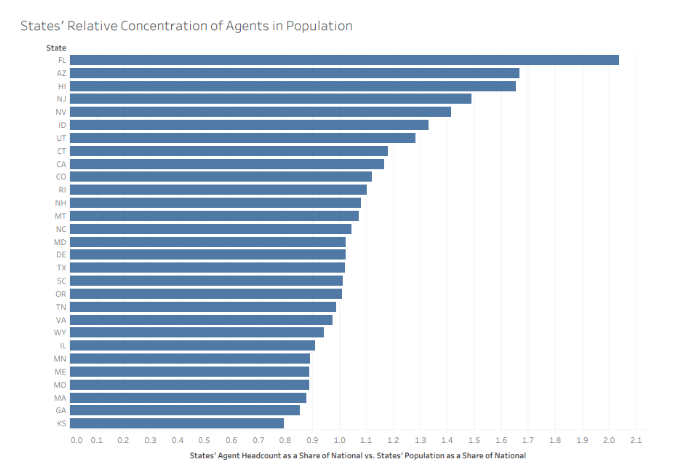

Where agents are more prevalent and why

Some states have much higher percentages of agents than others, relative to their populations. A state with an MLS in a high agent concentration location would likely deliver fewer listings per agent than in other states.

State residents’ likelihood to be real estate agents

Why are residents of some states more likely to be real estate agents than others?

High home prices correlate strongly with states that have high rates of real estate agents.

Logically, real estate agents in relatively low-priced communities must close far more transactions to earn the same income as an agent in a high-priced location. Local cost-of-living can make up for some of the variance that home prices have on agents’ income.

Agent competition tells the full story, though. The rewards of selling real estate in high-priced markets outweigh the costs of living in those markets, as evidenced by agent head counts versus total listing counts.

High home prices = more real estate agents

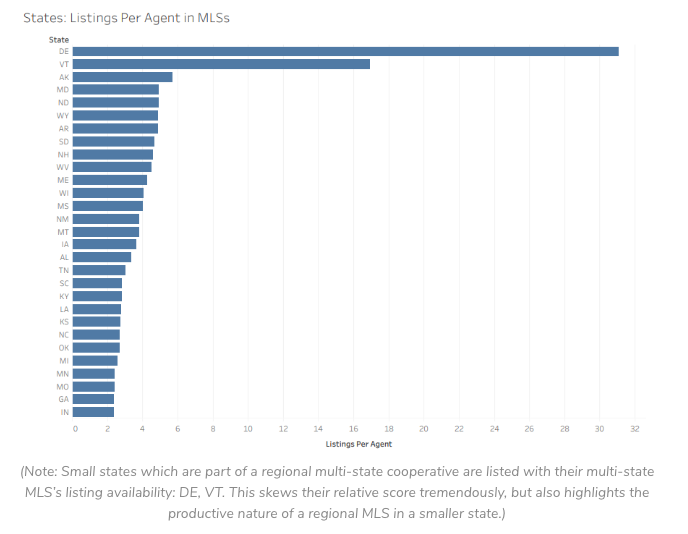

How many listing are available to agents?

Listings-to-agent measures can have great utility in analyzing how much value an MLS is providing in its market. Agent concentrations need to be taken into account when comparing markets with significant differences in home prices.

Available real estate listings for sale vs. number of real estate agents

The regional landscape

Analysis by region can be particularly useful for Realtor associations, as they are organized in this fashion within the national association’s reporting structure. They’re also heavily involved in the strategic vision for MLSs nationwide.

Listings available vs. number of MLS organizations, per NAR region

Regional figures are a valuable starting point for the industry to paint a picture of the overall landscape. Clarifying the regional situation allows for open conversations without identifying individual organizations as having positive or negative effects. This can lead to more granular discussions and introspective analysis over time.

Conclusions?

No conclusions about individual regions, states or MLS organizations are presented here. Real estate leaders have asked for an objective picture on nationwide trends and comparative data. This will initiate more informed conversations.

The geographies with higher rates of organizational overheard are not necessarily inefficient, but the statistics make it clear that additional analysis would be beneficial. The areas that appear efficient, in comparison, might still have significant opportunities for improvement.

MLS leadership: The big picture

The continual modernization of MLS infrastructure is being driven by organizations coming together to strategize over big-picture industry issues with quality information.

Good data creates a storyline that garners attention, awareness and buy-in from industry participants. Leaders from Realtor associations, MLSs, brokerages and technology partners can collaborate to create this environment.

The speed and the extent to which the MLS landscape will change beyond 2019 will be based largely upon these leaders’ ability to express the evolving needs of brokers, agents and consumers and to bring their constituents together with industry intelligence to act upon.

Editor’s note: For the current numbers and information on MLSs, see RESO’s MLS map and certification list.

Sam DeBord is Managing Broker/VP of Strategic Growth for Coldwell Banker Danforth, Past President of Seattle King County Realtors, and 2019 NAR President’s Liaison for MLS and Data Management. You can find his team at SeattleHome.com and Bellevu