- Most buyers don’t truly understand what goes into a fixer, including the costs, hassles and delays.

The lure of the fixer-upper is tempting for buyers. The “bargain” price of a fixer, compared to the price of an average house nearby, makes a real estate agent’s phone ring off the hook with showing requests.

The hard truth, however, is that fixers do not make sense for most buyers. An agent with a good grasp of all that is involved with a fixer purchase can be an invaluable resource as buyers weigh their options.

1. Most buyers don’t really know what a fixer is

To an agent, a fixer-upper is a train wreck. The discount price means big ticket system failures — roof, foundation, plumbing, electric — and fundamental repairs that must be dealt with before anything else.

They suck up money for what buyers are really dreaming of — flooring, countertops, lighting, cabinets, backsplashes and appliances — all the eye candy that they see on Houzz, Pinterest and HGTV.

2. The cost of renovation is high

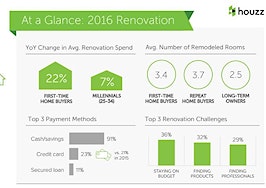

A modest bath redo or family room addition costs $100 to $200 a square foot, said Oliver Marks at HouseLogic.com.

For a kitchen renovation, Remodeling Magazine’s annual survey puts the national average cost at $59,999. A high-end kitchen remodel, HGTV estimates, is upward of $80,000.

In addition to labor and materials, renovation costs include architect and engineering fees, inspections and permit and licensing fees.

3. There are costly surprises more often than not

Even reliable, well-intended contractors cannot eyeball a project to the penny. Unanticipated repair costs of 10 percent to 25 percent are par for the course.

4. FHA 203k financing has delays and hassles such as paperwork, multiple inspections, review and more paperwork

The best contractors are busy, which makes coordinating with them for FHA-required estimates a huge headache.

The mortgage company and the appraiser must then take time to review the plans and sign off. In a competitive market, a buyer may lose out.

A seller may choose buyers with simpler financing and a quick close date rather than wait for the 203k buyer to jump through all the necessary hoops to get mortgage approval.

5. Buyers may run out of money

Lenders determine how much construction money they can lend using the difference between the purchase price and the appraiser’s estimate of market value after improvements.

Mortgage company guidelines further restrict how much money a buyer qualifies to receive.

For a home with a $190,000 sale price — even if the after-renovation value of the home is $315,000 — a buyer with 5 percent down may end up qualified to borrow only $47,500.

6. There are health and safety concerns

Old houses are full of dangerous toxins — including lead paint. Demolition and construction release harmful substances that can cause neurological and respiratory damage.

Children are particularly vulnerable. Construction zones should be sealed off. Harmful particles on clothes, hands and hair can migrate throughout the house.

The bottom line is that most people pay too much for fixers. Rarely do the costs of the renovations, when added to the sale price of the fixer, beat the sale price of the move-in ready house down the street.

After renovation, the buyer will have a custom house — exactly to their taste — but it won’t be a bargain.

A much better option than a fixer? “Grandma’s house.” Shag carpeting, old wallpaper, worn formica and old appliances are not hard to update.

Grandma likely took care of much of the routine maintenance. Fixers, on the other hand, have been neglected for years, causing significant issues that are costly to repair.

A good real estate agent can help the buyer find the better bargain. It is often cheaper to buy the more expensive house.

Zeta Cross is an agent with HG Realty Services in Philadelphia. Follow her on Facebook or Twitter.