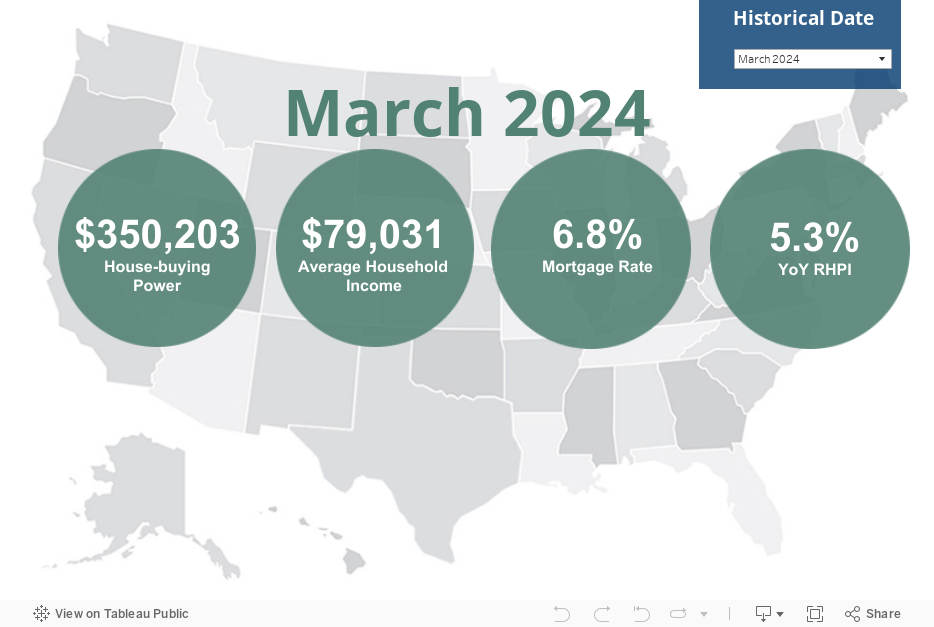

Houses were less affordable in March than a year ago, as home prices climbed faster than household income and mitigated the benefit of low interest rates, according to an index that measures housing affordability.

It’s the first decline in the First American Real House Price Index — which adjusts for the impact of income and interest rate changes on consumer’s homebuying power — since January, 2019.

With average household income rising 5.9 percent to $73,892 in March, and rates on 30-year fixed-rate mortgages hovering at 3.1 percent, the average American’s “house-buying power” was $502,031. That’s an increase of 10.9 percent from a year ago.

Source: First American Real House Price Index.

Mark Fleming | Photo credit: First American

But the index showed national home prices were up 14.8 percent from a year ago, “wiping out any affordability boost from rising house-buying power,” said First American Chief Economist Mark Fleming in a statement.

At the local level, affordability declined in 45 of 50 major markets, led by Kansas City, Missouri; Phoenix; Tampa, Florida; Seattle; and Austin, Texas. Kansas City was hit by a double whammy, as home prices were up by 16.5 percent, and annual household income declined by 4.3 percent.

Looking forward, Fleming noted that mortgage rates came down slightly in April, and have even dipped below 3 percent this month.

“House-buying power is likely to remain robust in the months to come, but affordability trends will likely hinge on changes in nominal house price appreciation,” Fleming said.

Another measure of home prices, the Radian Home Price Index, showed homes appreciating at an annual rate of 10.4 percent during April — the fastest growth since before the pandemic. Markets showing the strongest price growth included Boise, Idaho; Phoenix; and Charlotte, North Carolina.

The Radian Home Price Index pegs the national median home price at $277,356 at the end of April, up more than $20,000 since COVID lockdowns began in March 2020. Home price appreciation during that period has increased homeowner equity levels by more than $1.5 trillion dollars, Radian said.

Home prices in many markets are on the rise as buyers compete for scarce listings, and homebuilders struggle to catch up with demand. Some real estate agents are partnering with companies like Knock, Ribbon and Homeward, which let homeowners buy their next home before putting their existing homes on the market.

In their latest forecast, economists at Fannie Mae said they expect a gradual rise in rates over the next year and a half, with rates on 30-year fixed-rate mortgages averaging 3.5 percent by the final quarter of 2022.