This is the third installment of a new Inman series digging into, and explaining, routine real estate economic metrics and how they’re used to illuminate the current housing market and inventory crises. Don’t miss part 1, The Inman handbook on pending home sales, and part 2, The Inman handbook on new-home sales.

While pending-home sales and new-home sales help agents and consumers understand where the market is going, existing-home sales provide valuable insight into what’s happening currently in terms of price growth, supply and demand.

After record-high existing-home sales throughout 2020, sales have hit a three-month slump that has sparked concern among real estate professionals about buyers’ resilience in the midst of rock-bottom inventory, skyrocketing home price growth and bidding wars.

Although understandable, economists Mark Fleming of First American Financial Corporation, George Ratiu of realtor.com and Tendayi Kapfidze of LendingTree, said the current alarm over existing-home sales is ultimately rooted in a misunderstanding about properly contextualizing statistics and what they actually mean for agents, buyers and sellers as they make decisions.

Here’s what you need to know.

Table of Contents

- What’s an existing-home sale?

- The latest existing-home sales data and what it means

- Month-over-month vs year-over-year: What statistic matters more?

- Getting a full picture of existing-home sales

- What’s next for existing-home sales?

- Additional resources

What’s an existing-home sale?

The National Association of Realtors releases existing-home sales data by the 25th of each month. The report provides a snapshot of the previous month’s inventory, home sales pace and home price growth on a national and regional scale.

The report also provides statistics about average days on market, what segments of buyers are most active (e.g. first-time buyers, individual investors, second-time buyers), the percentage of distressed sales, sales and home price trends by housing type, and mortgage rates.

NAR Chief Economist Lawrence Yun also provides forward-looking statements about annual existing-home sales, home price growth and mortgage rates.

Real estate investing and financial education platform Investopedia considers existing-home sales a lagging indicator, which they define as an “observable or measurable factor that changes sometime after the economic, financial, or business variable with which it is correlated changes.”

Investopedia also said existing-home sales “confirm trends and changes in trends” versus pending-home sales and new-home sales that focus on how trends could develop in the upcoming months. Existing-home sales reports not only reflect the month at hand, Investopedia said, but completed pending sales from up to two months before.

“According to the National Association of Realtors (NAR), the reporting of most existing home sales transactions happens after the closing, and so does not consider pending sales still in contract,” the explainer read. “The majority of transactions usually involve a mortgage, which may take 30 to 60 days to close on.”

“As a result, existing home sale data most likely includes contracts that were signed at least a month or two before the report is published,” it added.

Lastly, NAR’s existing-homes report is based on transaction closings from Multiple Listing Services (MLS) and does not reflect sales trends outside of the MLS. “NAR re-benchmarks home sales periodically using other sources to assess overall home sales trends, including sales not reported by MLSs,” NAR explained.

The latest existing-home sales data and what it means

After increasing on a monthly and annual basis in January, existing-home sales have declined for three consecutive months — a trend that’s sparked concern among agents and consumers who worry bidding wars and declining inventory are finally getting the best of buyers.

In April, existing-home sales declined 2.7 percent month over month to a seasonally adjusted annual rate of 5.85 million, and due to the worsening imbalance between supply and demand, the median existing-home price for all housing types increased 19.1 percent annually to a record high of $341,600.

Although the market experienced a minor monthly boost in inventory (+10.5 percent) due to more homesellers placing their home on the market, it wasn’t enough to cool price growth as 88 percent of homes sold within one month.

Mark Fleming

First American Chief Economist Mark Fleming acknowledged the fear the latest declines have created. However, he’s focused on annual growth instead. “It’s the fourth-best April we’ve had in 15 years,” he said. “So the housing market is remaining amazingly resilient to all that has gone on over the last 12 to 16 months at this point, driven by the pandemic and the economic shock.”

Realtor.com Chief Economist George Ratiu said existing-home sales primarily reflect the tenacity of millennials and high-income professionals who’ve fled from the coasts to more affordable secondary markets, where their income can provide a better quality of life for less.

“It basically tells me that for many buyers, the combination of extremely tight inventory combined with the fact that prices, as NAR highlighted, were up almost 20 percent year over year, are really beginning to squeeze out first-time buyers,” he explained. “But the luxury segment has had triple digit gains from the prior year in sales.”

“So clearly here, the low financing costs, coupled with the fact that for many high-income professionals, remote work has been a real boon,” he added. “This past year, people have been able to save more money from the lack of a commute and be in a better financial position. Those factors have certainly incentivized those folks to continue buying.”

The flood of young professionals making the transition from renting to buying has become a two-edged sword for many markets, Fleming and Ratiu explained, as they spark bidding wars with locals who don’t have as well-lined pockets. Those bidding wars have expedited median existing-home price growth, which has risen at an unheard-of pace throughout the pandemic.

“There’s nuance in this,” Ratiu said. “I would say that what we’re seeing in the market right now reflects both home price appreciation and people pushing up prices through bidding wars.”

On the sell-side, Fleming said would-be homesellers are facing the consequences of bidding wars as well, which is reflected in the annual decline in existing-home sales inventory as sellers attempt to wait out the market. But this decision to wait is trapping would-be homesellers from reaching their housing dreams.

“This is a play on the old game theory Prisoner’s Dilemma,” he explained. “Ironically you’re a prisoner in your own home. You won’t sell because you’re afraid that you can’t find something to buy.”

“But, if all of the potential sellers out there chose to sell, there would be plenty of choices of things to buy,” he added. “But it’s really dangerous being the first one. Because what if everybody else doesn’t also sell?”

However, month-over-month inventory trends show sellers are deciding to make the jump as the country opens back up.

“We’ll see more inventory come to the market later this year as further COVID-19 vaccinations are administered and potential homesellers become more comfortable listing and showing their homes,” NAR Chief Economist Lawrence Yun said. “The falling number of homeowners in mortgage forbearance will also bring about more inventory [and] should cool down the torrid pace of price appreciation later in the year.”

Month-over-month vs year-over-year: What statistic matters more?

In conversations about existing-home sales and what they mean, Fleming, Ratiu and LendingTree Chief Economist Tendayi Kapfidze all noted consumers, real estate professionals and reporters often make two common mistakes: catastrophizing declines and improperly contextualizing monthly and annual trends.

All three men agreed that annual statistics are more reliable in understanding past and emerging trends than monthly statistics. Fleming said everyone should treat housing month-over-month statistics like daily stock market opens and closes.

“They tell you just because the stock market dips today, don’t pull out all your money,” he said. “So our equivalent of the daily movement is the monthly movement. On any given month, it could be a little up, it could be a little down, but one month does not make a trend.”

In a normal market, Fleming said three months is enough to begin considering a statistic or set of statistics a trend. However, he said the current market is anything but normal, as the pandemic has skewed 12 months of activity fueled by low mortgage rates, record migration, and other economic factors.

Furthermore, Ratiu said month-over-month statistics are more likely to reflect seasonal ups-and-downs rather than true shifts in median home prices, inventory or buyer activity.

“Traditionally, that’s very much the reason we use year over year sales, because in a healthy market sales tend to wane in the fall and winter months and then they get much stronger in the spring and peak in the summer months,” he said. “With that seasonality, it’s easier to look at year over year.”

George Ratiu

“The only caveat this year to yearly changes is that last year’s lockdowns were unprecedented in history, so for the next two more months, the year-over-year comparisons will have this asterisk next to them to say we’re comparing against an unprecedented period in the U.S. economy,” he added.

Beyond the battle between monthly and annual statistics, Kapfidze said national and regional trends should be seen as helpful starting points instead of a deciding factor when it comes to helping clients navigate markets.

“For the average consumer or even the average buyer, you shouldn’t focus too much on what the level of sales is in nationally reported statistics because really, what matters for you, as a buyer or seller is much more what’s going on in your local market,” he explained. “[Nationally reported statistics] are more important for people like lenders, builders and larger businesses.”

“It matters much more what’s happening in your local areas, but these reports are good information to have only because it contextualizes the overall macro situation,” he added. “However, I don’t think it’s information that should influence any individual buyer or sellers’ housing decisions.”

Getting a full picture of existing-home sales

Although NAR’s existing-home sales report is a reliable first step in understanding existing-home sales and the real estate market as a whole, Fleming, Ratiu and Kapfidze all said real estate professionals and consumers should dive into additional reports to have a better lay of the land.

When it comes to understanding home price growth, Ratiu said consumers should look at weekly updates provided by home search platforms and brokerages, such as realtor.com, Zillow, Redfin and others. He also encouraged consumers to look at the Case-Shiller Price Index, which better reflects price growth minus inflation caused by bidding wars.

“What’s important for people to distinguish is the Case Shiller Price Index tracks the same home over time to measure price gain, in a sense, trying to avoid what’s common to most other indices, which is the product mix,” he said. “So let’s say one month, a huge number of luxury homes come on the market, the median price will rise simply because more expensive homes are being sold.”

“Conversely, if you have lower priced homes flood the market in one month, you’re going to see median prices possibly [go] lower,” he added. “Case Shiller eliminates that by looking at the same homes over time as they change hands.”

Tendayi Kapfidze

On the other side, Kapfidze encouraged agents, especially the more than 80,000 real estate rookies who joined NAR in 2020, to take advantage of MLS data and other aggregate data sources available exclusively to them to contextualize and personalize what’s happening on a national or regional scale.

“If you are an agent, it is important for you to have context around what is happening in the industry and what the marketplace is doing. You want to understand things like the existing-home sales and new-home sales reports,” he said. “You definitely want to have that macro contextual information, but when it comes to transactions, the most important thing is to understand your local market dynamics.”

From there, Kapfidze said, agents can create dynamic and easy-to-understand reports for buyers and sellers who want to know what national, regional and local data mean for them and their housing decisions.

What’s next for existing-home sales?

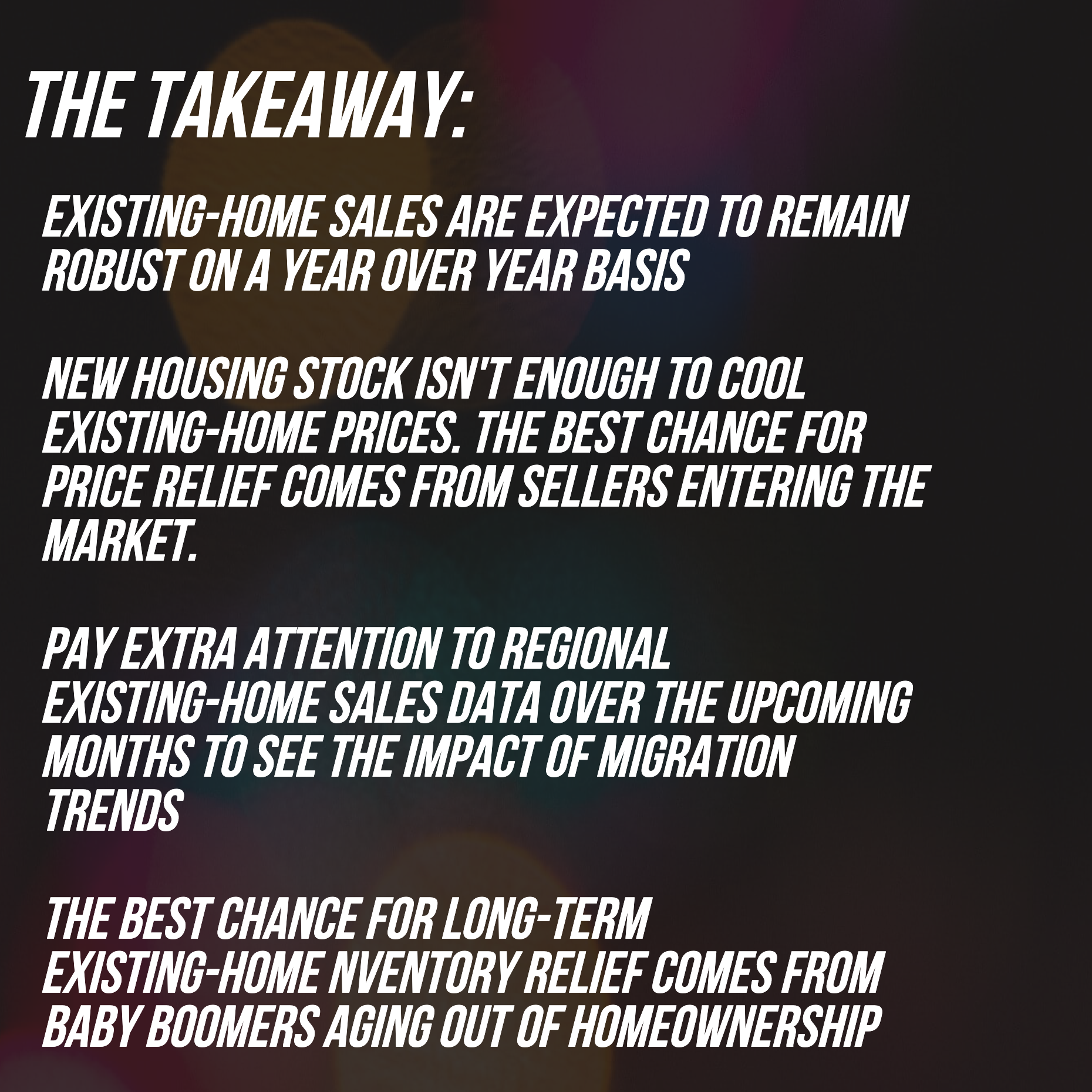

All three economists expect existing-home sales to stay robust on a year over year basis, especially if mortgage rates remain favorable and employers continue to embrace remote working. However, inventory shortages will continue to be a major barrier.

“Even if we have lots and lots of new homes for sale, it’s only 10 percent of the market,” Fleming said of the hope an influx of new homes will cool existing-home price growth. “It would take an unprecedented amount of homebuilding to make up for the shortage of overall supply of housing in the United States.”

“We’ve under-built the housing stock for the last decade, to the tune of millions of homes,” he added. “So yes, it’s important as a relief valve to the inventory shortage, but I have a hard time seeing that it’s the panacea.”

Kapfidze said the best hope for homebuyers is more homesellers entering the market, which seems to be the case based on the 10.5 percent increase in listings from March.

“Maybe some people who weren’t comfortable putting their homes in the market because of COVID will put their homes on the market now,” he said. “A lot of people over the past year — because of the uncertainty around COVID, the economy and their own individual financial and employment situations — have been reluctant to introduce the added volatility of selling their home.”

“As things get back to normal, more people will list their homes,” he added.

Going forward, Fleming encouraged people to pay more attention to NAR’s regional existing-home sales data as it will give people a starting point for understanding how the pandemic shifted pockets of exorbitant price growth from the coasts to places like Oklahoma City, Dallas and Nashville.

“[Coastal buyers] are seeking the affordability,” he said. “We call it arbitrage — you sell your expensive home in Southern California and you can buy a mansion in Oklahoma City. They’re seeking that opportunity and will continue to do so.”

Fleming also said generational trends, such as millennials aging into homeownership, baby boomers aging out of homeownership or the rising formation of multi-generational households, will continue to have an impact on existing-home sales.

“A lot of that stock that would be potentially inventory for sale is owned and lived in by baby boomers at the moment, and so the question then becomes when do they age out of becoming a homeowner and move into the next phase of their life?” he said. “Keep in mind, that’s a lot of stock because baby boomers are a very big generation.”

“That’s where the relief is going to come from: when baby boomers eventually start to age out and all of a sudden, they’re no longer the existing homeowner making the contemporaneous buying decision,” he added. “But that’s a pretty slow-moving demographic process and certainly not fast enough for millennials.”