- Housing prices will fall, but the inventory crisis will finally end.

- Realogy will launch low-cost brokerage and franchise options.

- Zillow will beat Upstream at its upstream game.

- Opendoor will become the most important company in real estate.

- Brokerages will begin to promote younger executives.

- NAR will do something about subpar agents and will name a female successor to CEO Dale Stinton.

It turns out that last year, despite my predictions being mostly wrong, no one got a refund from Inman…especially since Amber Taufen, the editor, pretty much said no one is getting their money back.

As a result, Inman was good enough to try this again for a second year in a row.

I appreciate that very much, guys, since there’s a special frisson of excitement when predictions are proven so wrong in front of so many more people than are on my little industry blog. As someone — not me, but someone, I’m sure — likes to say, if you’re going to fail, then fail big, son!

I would like to point out that I suffered for this year’s post.

Primarily because in order to select the accompanying music videos to these seven predictions, I had to comb through hours of music by ‘N Sync, Backstreet Boys, One Direction, 98 Degrees (I had blissfully forgotten that Nick Lachey even existed for several years) and others.

I hope you can appreciate my sacrifice, especially since YouTube now thinks I’m super into boy bands and constantly suggests something or another from O-Town and LFO….

Without further ado, let’s get into predictions sure to be wrong, or your money back!

(Editor’s note: And once again, let me remind everyone that this is Inman, not Rob’s little free blog — so no, there will be no money-back guarantee this year, either.)

1. Housing prices fall, but inventory crisis ends

(This song and prediction are dedicated to my Democrat friends…. I’m pouring one out for y’all.)

As you read this section, please remember that I look like a famous economist but am, in fact, not one myself. Hallelujah!

One of the least expected events of 2016 has to be the election of Donald Trump as president of the United States.

I don’t think even Trump expected to win, and win so handily. But win he did, and among other things, he wrecked one of my 2016 predictions: Spencer Rascoff as Secretary of the Department of Housing and Urban Development.

Instead, we have Dr. Ben Carson, whose experience with housing is having lived in them. Then again, he is a Yale graduate and a brilliant neurosurgeon, so I’m sure he can figure things out pretty quickly with smart people under him.

(Hey Secretary Carson, if you’re reading this, I can help you figure this industry out… #justsayin….)

At the same time, we have seen what’s been called a “affordability crisis” in housing over the last few years.

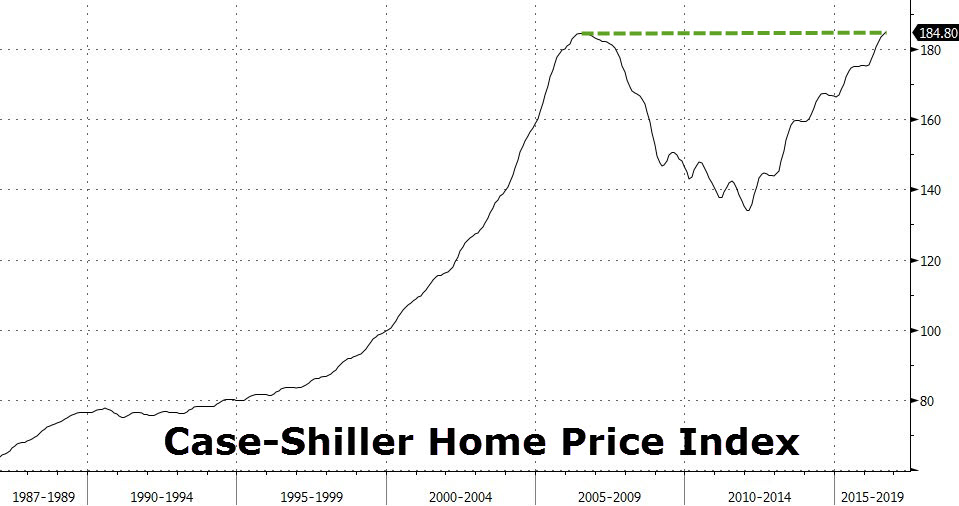

Prices are skyrocketing compared to wage growth: Bloomberg reports that home prices are going up 13 times faster than wages are.

And Zerohedge (admittedly a doom-porn blog, but often insightful) notes that home prices have matched where they were at the peak of the Housing Bubble in 2006:

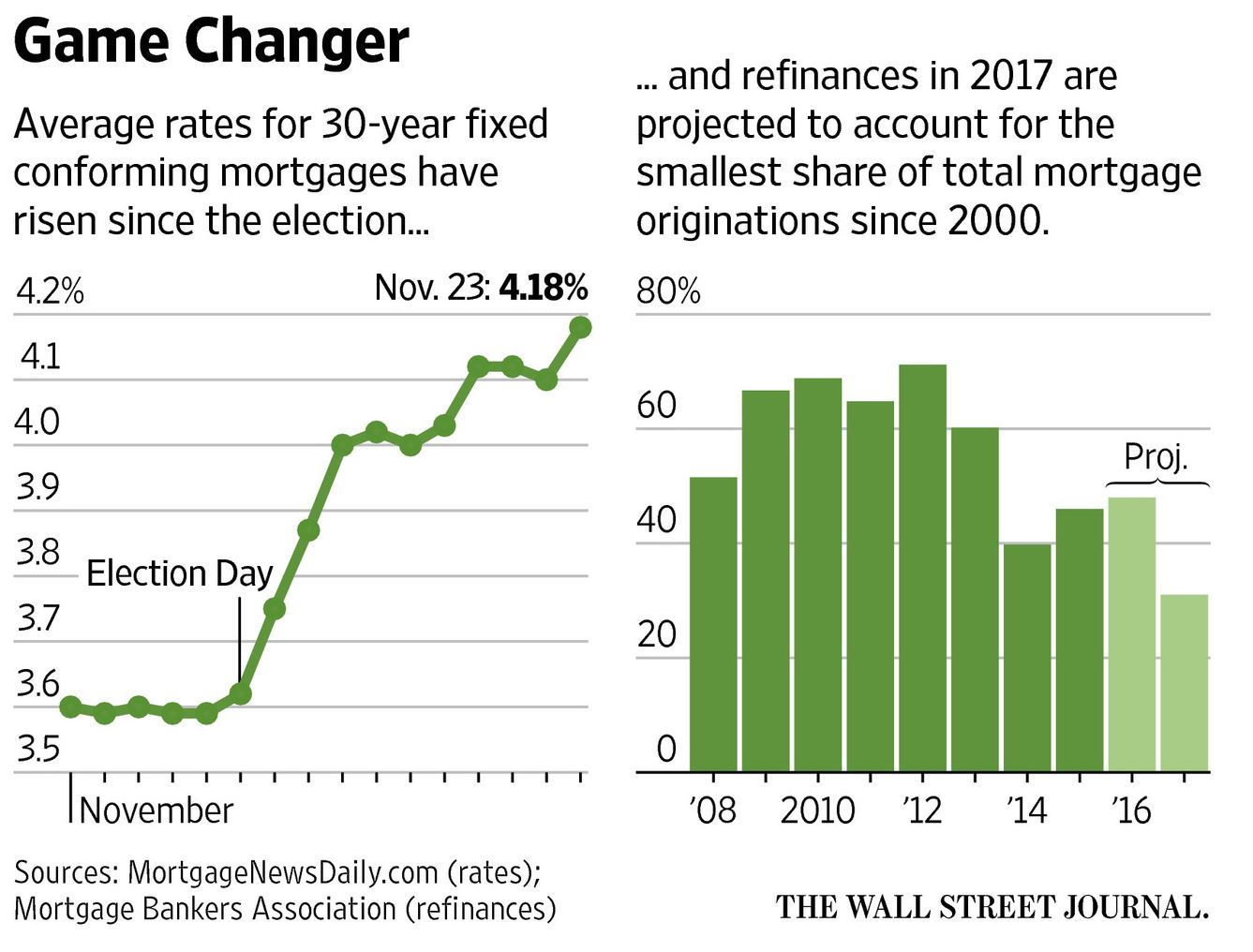

Now, maybe it’s coincidence, or it’s the Bavarian Illuminati and the Trilateral Commission working against the Trumpening, but we have seen what some people are calling “Trumpflation” since the election:

As a result, quite a few economists and industry watchers are predicting that buyer demand will drop significantly in 2017 simply because fewer of them can actually afford to buy.

So I’m going to jump on that bandwagon and say that home prices will drop significantly by the end of 2017.

Do I have to pick a number? Dammit. Umm… let’s go with 20 percent drop in median existing home prices by December of 2017 — a figure I just pulled out of my nether regions.

At the same time, however, I think we see an end to the inventory crisis.

Economists and experts can’t quite agree on the cause for low inventory — after all, home prices are at all-time high and interest rates were at historical lows, so what gives? Some blame investor activity, some blame “pocket listings”, while others talk about millennials embracing the “on demand economy” of Uber, Zipcars and rentals.

But most serious economists agree that a major cause of inventory shortage is the lack of new construction.

Redfin echoed their sentiments in a post in February of this year:

U.S. homebuilders built an average of 1.5 million homes each year for the 50 year period preceding the housing collapse. Home construction took a nosedive in 2008 and still hasn’t recovered.

The U.S. needs about 1.2 million new housing units a year to keep pace with population growth and another 300,000 to replenish homes that are demolished every year.

That translates to a total of 12 million houses, condominiums and apartments that should have been built over the last eight years. Instead we’ve built only half as many, and most of that construction has been apartments for rent instead of homes for sale.

Builders are starting to ramp up, but it will take years to close that 5.5 million gap.

Why might builders be so lackadaisical about building homes? I mean, isn’t that how they make money? Build homes and sell them?

Two oft-cited reasons are (a) difficulty of getting building permits, especially in certain urban areas, and (b) difficulty of getting construction financing.

Given that we have elected a president who built (ahem) his fortune in construction, who ran on a platform of blue collar jobs (of which construction is a big component), who has filled his cabinet with people who dislike government regulation, and is theoretically of the same party as the one that controls Congress — a party that supposedly is about free enterprise, though recent behavior would temper such faith — we could see the Trump administration launch programs geared towards encouraging/subsidizing construction.

For example, the Trump White House might apply all kinds of pressure to cities that have building-unfriendly policies to relax them a bunch and issue permits like there’s no tomorrow. (“So hey, San Francisco, you like your Federal road grant dollars, do you?”) Maybe they shift gears away from subsidizing residential mortgages (see, for example, Fannie and Freddie) and towards subsidizing construction loans to builders.

Who knows with this guy? The sky is the limit.

In any event, my first prediction sure to be wrong or your money back, I’m going with house prices falling by 20 percent and inventory crisis easing up across the country.

2. Realogy launches low-cost brokerage and franchise operations

I have been discussing Realogy since the very first days of this blog. Here’s a post from 2008 as an example.

Since I started my adventures in real estate with a stint at Realogy, I have long had a soft spot in my heart for the company, and an enormous amount of respect for some of the talented folks there.

But the latest quarterly earnings in Q3 of 2016 held a few eye-opening surprises for me.

Second, Realogy has quietly acknowledged some “challenges” that I noted back in 2012 in a report called “Realogy Rides Again: 2012 Results and Future of Real Estate Brokerage.” (It was “premium content” back then, so if you want a copy, email me.) In it, I wrote the following:

Empowered by technology that is getting better, faster, and cheaper by the day, the agent team concept has taken hold within the agent community. It is starting to dominate the conversation. As yet, traditional brokerages have not solved that riddle, and the agent team is an existential threat.

Bottomline is that Realogy performed extremely well in 2012. Investors may rightly wonder if the stock price is not overvalued given that Realogy still hasn’t produced net income for years and years, and the debt is still at over $4 billion. My read is that the core operations are extremely strong, and that Realogy has certain strategic advantages due to its size, scale, technology, and operational discipline. Nonetheless, investors probably should be concerned about whether Realogy can maintain its agent commission costs, which rose in 2012, in light of industry developments around agent teams and technology. [Emphasis added]

That was four years ago. Every single quarter since then, Realogy has discussed its efforts to deal with agent commission margins, even as they got worse and worse.

The typical response by Realogy executives over that time was to say that NRT was making some changes, doing some tweaks, trying a few tricks to improve margins, and they expect those actions to bear fruit. Except those actions really haven’t borne any fruit….

Well, in the fall of 2016, Richard Smith, CEO of Realogy, said this in the earnings call:

As we discussed on our second-quarter call, NRT has been facing two significant operating challenges: strong competition for our top-producing agents and soft demand at the high end of the housing market. Again as we expected, those challenges continued to influence NRT’s performance in the third quarter.

We made a number of changes in NRT during the third quarter, including the creation of new executive roles created to focus on growth, maximize the efficiency of its operations, and to provide enhanced value and service levels for its agents and consumers.

We created the position of Chief Strategy & Operating Officer for NRT to assist CEO Bruce Zipf in executing its new growth and efficiency initiatives.

We appointed Ryan Gorman, a 12-year veteran of Realogy to the role. Ryan played an integral part in the acquisition of ZipRealty and NRT’s recent adjacent growth initiative into property management, which under Ryan’s leadership has grown to over 26,000 single-family homes under management.

The major focus for NRT is to more rapidly grow its independent sales associate base as well as increase the productivity and retention of existing sales associates. With that in mind NRT created the role of Chief Recruiting Officer in the third quarter appointing Peter Sobeck who most recently served as the Chief Operating Officer for our Citi Habitats subsidiary in New York City. Peter is working with field leadership to organize and execute an aggressive campaign to increase our recruitment of top producing independent sales agents and their agent teams, and to enhance NRT’s existing agent retention and productivity programs.

…

NRT also continues to invest in its agent value proposition and recently promoted a seasoned operating executive, Monty Smith, to the new role of President of Company Generated Business. The position is responsible for all activities that produce Company generated leads, which accounted for approximately 10 percent of NRT’s closed business including leads from relocation and Internet lead service centers as well as NRT’s ZipRealty operations. [Emphasis added]

This is about as close to admitting that they’ve got real serious problems as you’re going to get from a public company CEO on a phone call with Wall Street analysts.

Public companies do not create three senior C-level positions in a $4 billion a year company for fun. They do it because they really need to turn the ship around. And further hints come from the Q&A, where Richard says this:

Although we would like to and are currently in the process of creating even a stronger value proposition for teams, teams often fall in lower categories. But the very high end of the market is all about the economics of the relationship between us and the agent. And that is where our primary focus is right now.

Agent splits are a big part of the calculations, as is evident from this exchange:

Anthony Paolone – JPMorgan – Analyst

And then in terms of the business initiatives, can you talk — can you split it between what you think happens to splits and how you kind of fortify NRT with just perhaps offering better splits to the agents versus other types of costs that are being spent to improve competitiveness?

Tony Hull – Realogy Holdings Corp. – EVP, CFO & Treasurer

It is a combination of getting — looking sort of market by market at being more competitive on splits, so that is a very laser focused activity that NRT has already done in three or four of their markets and will continue to do in more of their markets over time. So you are seeing the effects of that on split today to some extent.

But to the other part of the — we are a full service broker and we want to enhance the value proposition we provide to agents. And obviously we have 47,000 agents who think the value proposition is very strong and the company generates $4.4 billion of revenue.

So we think we have a rock solid foundation. But we always can improve on things like coaching and training and more leads and more lead conversion, better marketing tools and that sort of thing. So it is really a combination of the two. [Emphasis added]

With all of that in mind, I predict that Realogy will launch a true low-cost operation in 2017.

Sure, they might try everything else first, but to me, they’ve already tried everything else over the past sixteen quarters since the end of 2012. And while they acknowledge the depth of the challenge now and have made senior appointments to try and address it, they also know that Keller Williams is growing like gangbusters with 152,000 agents in 2016.

I personally know a number of NRT operators, from office manager up to regional Presidents — they’re really good, really savvy, with great leadership and great skills.

But they’re stuck in a business model that really hasn’t been updated in decades, despite the changes to technology and the market. They fight with one hand tied behind their backs, and a big part of the issue is the cost structure of the full-service brokerage operations that is the NRT.

Similarly, on the franchise side, there are some amazing Realogy franchisees who are successful, dominate their markets and are killing it.

But they’re doing all of that with a headwind of a franchise model that can be as high as 8 percent of gross commission income (6 percent as royalty, 2 percent as National Advertising Fund). And again, changes in technology and agent behavior mean that those headwinds get stronger, not weaker, by the day.

I have some ideas on what/how/where Realogy might do such a thing…but for now, let’s just keep it with predicting that Realogy will either launch test models or buy existing low-cost models (for example, Realty One, HomeSmart, Nexthome, United Real Estate and so on) to diversify its offerings not only to agents and agent teams, but to brokerages who are or could be their franchisees.

Remember, I predicted (wrongly, yay!) last year that Realogy would acquire HomeSmart. Maybe this year….

Because they have to at some point; might as well be sooner rather than later.

3. Zillow goes upstream of Upstream

(Note: I have a business relationship with Zillow. But they don’t know I’m writing this, ’cause they never do.)

Last year, I predicted that Upstream would launch and get major traction. That was of course proven to be wrong, as all of these predictions are guaranteed to be.

What was a bit surprising, though, was the extent to which Upstream did not get traction.

I wrote last year that the combination of large brokers and the National Association of Realtors (NAR) would prove irresistible to MLSs, which would feel immense political pressure to get on board the Upstream train:

The technology is not, has never been and will never be the barrier to progress in real estate. Slow decision-making, political infighting and need for consensus-building are, have been and will be the problems.

Thing about Upstream, though, is that it has near-universal support from the largest companies in real estate.

Sure, said support might be somewhat lukewarm (as in the case of Realogy), but there are enough passionate supporters with very deep pockets and hundreds of thousands of Realtors as in the case of HomeServices of America, The Realty Alliance, Keller Williams, Re/Max and others who can manufacture consent if necessary.

Add to the fact that NAR has lined up behind Upstream and all of the associations get taken out of the picture in terms of rebelliousness. Some MLSs might drag their feet because they remember that the origin of Upstream was as a nuclear option to be used against recalcitrant MLSs, and they remember that the origin of RPR was as a single national MLS.

But when big brokers and NAR are calling the shots, MLSs will have little choice but to comply — at least if the MLS CEO likes having that job.

So I predict that Upstream will actually go live by the second half of 2016, propelled forward by the incredibly political will of the large brokerages and the need for NAR to showcase some sort of major success with its enormous investment into RPR.

That prediction is about as correct as all of the pundits predicting a landslide victory for Hillary in 2016. Seemed reasonable, seemed correct — was dead wrong.

Turns out, large brokerages are not nearly as united as I had imagined, and NAR isn’t necessarily perceived as a friend by the MLS community.

Instead, in 2016 we saw Zillow acquire Bridge Interactive, thereby putting together every piece of the Upstream puzzle, except for the unwieldy bureaucracies and the unworkable governance structures of Upstream. (Although having Alex Lange as CEO will help with the operations of Upstream itself, since he is a capable guy.)

Between Bridge, Retsly, dotloop and its other technology products, Zillow is now able to deliver on all of the publicly-stated goals of Upstream:

- Single point of entry

- Streamlined data management

- Control over data distribution

And the success of Errol Samuelson and his team at Zillow’s Industry Relations throughout 2016 suggests that while haters gonna hate, more and more MLS executives and board members are no longer thinking of Zillow as Satan Incarnate. (It’s hard to keep on holding up Zillow as the bogeyman when it hasn’t bogeyed in the decade or so since its founding, and guys like Opendoor and Reali are actually out there with huge amounts of funding.)

So as we enter 2017, we still have Upstream standing by its original timeframe with 15 brokers in pilots with five MLSs. Meanwhile, Bridge has systems already live in production across the MLS and brokerage landscape, and Retsly is live in production and vendors are using it to pull data from the MLS via a simple API, and Zillow has all kinds of data its websites and mobile apps generate to feed the beast.

I’m now predicting that Zillow goes upstream of Upstream and deploys all of the functionality that brokers say they want from Upstream long before Upstream finishes its pilot/beta-testing. Again, sure to be wrong, but hey, there you have it.

4. Opendoor emerges as the most important company in real estate

I’ve been talking about Opendoor for two years now. I thought it was the most interesting company when it launched, and over time, I began to think it’s the most disruptive thing to hit the larger American real estate industry since…I don’t know…the Internet itself?

In my last post about Opendoor, I pointed out that it is quite unlikely that the company raised $720 million in debt and equity to get into the real estate brokerage business:

I could be wrong, of course, but… really, really smart people at venture funds and hedge funds and private equity funds put $720 million into Opendoor. Maybe it’s for a piece of the $71 billion in commissions. Maybe.

I’m betting that it’s for a piece of the $61 trillion (number not guaranteed to be correct) profits of the banks from residential mortgages.

So yeah, I think Opendoor is about revolutionizing the entire culture around how homes get bought and sold in the United States by replacing the broken mortgage financing system with an institutional market maker system. Do that, and you can’t help but impact the pain-in-the-ass homebuying and selling system since the latter rides on the shoulders of the former.

If it pulls this off, Opendoor will become the single most important company in real estate. Hell, it could become the single most important company in banking, in much the same way that Uber has become the single most important company in transportation and logistics, not just in taxi and black car industries.

And you know what? With a new political environment in Washington, D.C., and $720 million in funding, I think Opendoor pulls it off.

The proof will be if Opendoor starts offering some sort of institutional seller-financing option to buyers that is free of most of the bullcrap that infests the mortgage application process. Because they can’t offer that without having the private-label mortgage-backed security (MBS) pipeline in place, which means we’ll see that first Opendoor residential MBS within a few months.

So let me paraphrase Blackstreet, street poets in matching white overalls…

OD get down, good lord

Baby got ’em up open all over town

Strictly biz, they don’t play around

Cover much ground, got game by the pound

Getting paid is their forte

Each and every day, true player way

I can’t get ’em out of my mind (WOW!)

I think about Opendoor all the time (WOW, WOW!)

No diggity, no doubt.

5. The youth movement begins in brokerage

In the 2015 edition of Swanepoel Trends Report, I helped write a chapter on “The Coming Leadership Retirement Wave” and the importance of succession planning. Maybe that played a small role, though it’s more likely that Stefan’s globetrotting and far more important voice telling brokerage owners and CEOs that they need to start thinking about a succession plan played a far larger role.

Either way, I have heard more and more conversation about some of the Great Old Lions of the industry starting to step back, take a more passive role and grooming younger leaders for the top job.

We haven’t seen it actually happen, however. The only CEO under 40 in the top 20 brokerages in Real Trends 500 is Kuba Jewgieniew, who got there because he started the brokerage himself (Realty One). (To be fair, Matt Widdows of Homesmart is only 44, but then, he also started his brokerage that grew into the Top 20.)

The mainline old guard brokerages have CEOs well into the late 50s or older. Since I suspect that many of them are under the same pressures as Realogy’s NRT unit is (See no. 1 above), some of the Great Old Lions may realize that they may no longer be the right ones to tackle those challenges. They’ve earned their place, their legacy, their wealth, and it may be time to pass the baton to a young buck hungry to prove herself.

There are a number of younger leaders in the brokerage world in that second-tier just below CEO. And there are hundreds, if not thousands, of people climbing the ladder in brokerages and real estate companies across the country in midlevel management positions. Many are being groomed for future leadership, but there are those who are ready today.

I think 2017 is when we see the youth movement begin for real, with some iconic figures in the industry stepping down and passing the torch.

To be bold, I’m going to predict that we will see someone under 40 become the CEO of a Top 100 Brokerage by Volume (that he didn’t start himself), and at least a half dozen CEOs under 50 by the end of 2017.

6. NAR does something about the crappy agent problem

It’s going on 19 months since NAR released the DANGER Report, in which the A1 Danger was:

Since then, we have seen bupkis and squadoosh from anyone that actually matters about what to actually do about Danger A1. Sure, we’ve had that Code of Excellence thing in 2014, but…well, it’s one o’ dem aspirational things, you see? And an aspirational Code is not a Code at all, but a suggestion, sort of like the traffic “laws” in Shanghai. (I know this from personal experience in taxicabs in Shanghai — something I plan never to repeat again in this lifetime.)

Anyhoo…I am predicting that changes in 2017. Sure, I happen to know a thing or two about things coming down the pike from people deeply involved with a large organization that starts with the letter “N” and ends with the letters “ational Association of Realtors” so I have an edge in the prediction game…but still….

I think we see a significant step forward in terms of ethics, competence, requirements for advocacy and the all-important requirement to be dedicated to the art and craft of representing consumers in the largest transactions of their lives.

I’ll go out on a limb and predict that this time, it won’t be an aspirational suggestion, but an actual enforceable requirement. You know…a code.

All I can say to that is…quit playing games with my heart, and let’s get this done for the industry, for the great brokers and agents out there, and for consumers everywhere who deserve better.

7. NAR names a female successor to Dale Stinton

I’m just going to repost this entire prediction from 2016, because… well, I didn’t realize that the NAR selection committee doesn’t even get named until the end of 2016.

So this will happen in 2017. Everything else remains the same as I wrote previously, except that I’ve changed my “outside the industry” pick.

As far as I know, Carly Fiorina is unemployed. And given how she went after The Donald during the primaries as Ted Cruz’s running mate, I kind of get the feeling she won’t be in government or in the GOP party machinery anytime soon.

Clearly, she knows politics, knows how to manage large complex organizations, and understands technology (as the former CEO of Hewlett Packard). I’m personally fond of her because (a) she has a degree in useless majors like Philosophy and Medieval History, (b) she was born in Texas, and (c) she worked as a real estate broker at Marcus & Millichap.

If NAR isn’t going to pick one of the many extremely capable women from within the industry, it should take a look at Carly. I have no idea if she wears Abercrombie & Fitch, however, but if she were a bit younger, I’d bet she would.

Conclusion

Well, first, thanks for reading all 4,000-plus words. You’re either really dedicated or really bored. Either way, thank you. As our new president might say, “I love bored people! They’re my biggest supporters!”

Second, looking through the above seven, they don’t strike me as particularly dark and scary — as some of mine were in past years.

I blame it on Belize, Panty Rippers, sun and surf, bike rides in the sun, and…wait, no, no, no. Belize was awful. Don’t ever go there. Only acid rain, dark storm clouds and gale-force winds blowing insects directly up your nostrils — and the water is filled with man (and plankton) eating sharks that have a special hankering for Norteamericano meat. I’m glad to have escaped barely with my life and most of my sanity.

Third, I apologize. Truly, mea culpa. I probably did you a grievous wrong. But One Direction just had to be used in this post.

Happy 2017 everybody!

Robert Hahn is the Managing Partner of 7DS Associates, a marketing, technology and strategy consultancy focusing on the real estate industry. Check out his personal blog, The Notorious R.O.B. or find him on Twitter: @robhahn.