- Millennials are typically marrying and having kids later in life -- after securing a college degree.

- Stagnant income growth and lingering concerns from the recession are also impacting homeownership.

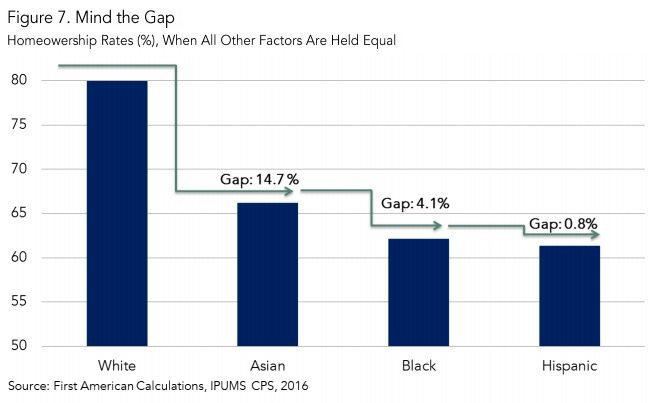

- Even controlling for other factors, the gap between white and Asian, black and Hispanic homeownership exists.

When the rate of homeownership is at a 50-year low, but people of all ages and ethnic backgrounds continue to say that owning a home is part of their American dream, it’s no wonder that real estate agents and brokers have questions about the future of homeownership.

Mark Fleming and Odeta Kushi, economists at First American Financial Corporation, dug deep into the motivations and challenges of today’s homebuyer for a new study, “Six Trends Poised to Reshape Homeownership Demand.” As millennials — potentially the largest-ever generation of homebuyers — come of age, their needs and lifestyles are going to influence what buyers want.

“While it may not be a surprise that homeownership remains a priority, it may come as a surprise that millennials have not been discouraged from this goal,” Fleming and Kushi write. “Millennials are often referred to as a ‘renter generation,’ because they have prioritized their education and tend to concentrate in metropolitan areas.

“But the American dream is not the mere act of owning a home, but rather an ethos or set of ideals that allows citizens the opportunity to pursue prosperity and upward mobility through hard work,” they added. “In this context, homeownership is not just about shelter, but a primary vehicle for wealth creation for middleclass Americans.”

Millennials are educated

Are you buying into the myth that millennials are “over-educated and underemployed?” That education has its upside, friend.

“A millennial with a college degree earns approximately $17,500 a year more than a millennial with only a high school diploma,” noted Fleming and Kushi — so those millennials are also better placed to buy homes.

First American looked at the share of individuals who earned bachelor’s degrees and the corresponding increase in ownership.

“Between 1992 and 2005, the increasing share of individuals earning bachelor’s degrees corresponded with a 2.7 percent increase in homeownership,” Fleming and Kushi wrote. “Between 2005 and 2015, partially in response to the Great Recession and slow economic recovery, millennials have been staying in school. Consequently, the educational attainment rate, which measures the completion of degrees, declined. All else held constant, this caused modest year-over-year declines in the homeownership rate.

“In 2016, a jump in the educational attainment rate drove a 3 percent year-over-year gain in homeownership,” the economists added.

Fleming and Kushi also included some numbers from Pew Research Center that indicate how millennials feel about education:

- 19 percent of millennials have already graduated from college

- 44 percent of millennials plan to graduate from college

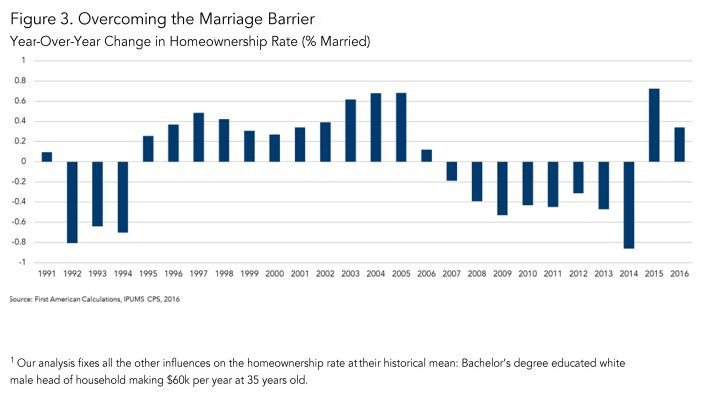

Getting married

Graduating from college in order to land a good job is only part of the equation, Fleming and Kushi noted. Many wait to buy until they feel they’re ready to “settle down,” and as the economists pointed out, “settling down” might mean something different to a millennial than it did to a baby boomer.

“The homeownership rate is 30 percent higher among married couples than other households,” Fleming and Kushi wrote — and marital rates are falling; the share of adults aged 24 to 34 that are married fell to 54 percent in 2014 from 70 percent in 1995.

The economists said that marriage was a net contributor to homeownership between 1995 and 2005 as Generation X tied the knot, “but from 2005 to 2014 the declining marriage rate alone has reduced the homeownership rate by 3.5 percentage points,” they wrote.

“This trend turned around in 2015, with marriage being a contributor to homeownership in 2015 and 2016,” they added. This indicates that millennials are getting on the marriage train … just a bit later in life than their generational counterparts.

Having babies

If you’re not living a child-free lifestyle, the next step after marriage typically involves having a kid or two. Millennials are also delaying the decision to reproduce — and that has consequences for homeownership, according to First American.

“As one might suspect, the more children in a household, the more likely the decision to own versus rent,” wrote Fleming and Kushi. The homeownership rate is 1.7 percent higher for households with one or two children compared to households with no children, and it is 5.4 percent higher for households with three or more children.”

The economists expect family growth to follow the same pattern as marriage and say that as millennials start to have kids (later in life than other generations did), real estate agents and brokers can expect this age group to get more serious about buying a home.

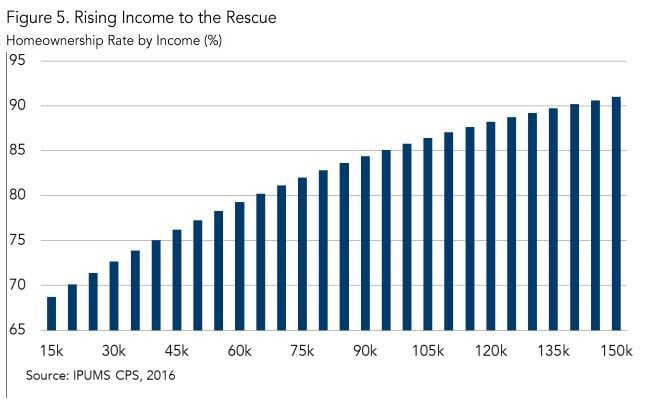

Income growth

When wages aren’t growing and home prices are, it’s easy to see how homeownership gets caught in the crossfire. Buyers can’t save for a down payment and sellers can’t consider moving into a bigger space if they aren’t getting raises at work or finding better paying jobs elsewhere.

“As one might expect, homeownership increases as household real incomes increase,” wrote Fleming and Kushi. “For a household earning $50,000, an extra $10,000 a year would increase the likelihood of homeownership by 2.1 percent. Going from an income of $50,000 to $100,000 increases the likelihood of homeownership by approximately 10 percent.”

There’s been an uptick in income growth, according to Fleming and Kushi — and that’s good news for agents and brokers.

There’s been an uptick in income growth, according to Fleming and Kushi — and that’s good news for agents and brokers.

“After a period of stagnant wage growth, median household income in the United States increased from $53,718 in 2014 to $56,516 in 2016,” they wrote. “This upward trend in income translates, all other factors held equal, to an almost 1 percent rise in the likelihood of homeownership.”

And a lot of that wage growth and job creation is happening for millennials in particular, they added.

It’s the economy

Job security has a lot to do with whether or not a potential buyer is willing to take the plunge — and that doesn’t just mean keeping a job; it also includes getting a job or changing a job. So the overall economy — in addition to mortgage rates, home prices and other economic indicators — has a profound effect on whether or not buyers and sellers are buying and selling.

The economy is only recently recovering from a recession, as many real estate agents well remember, and as the country gets back on its feet financially, First American thinks that the demand for homeownership is going to grow.

“It’s hard to predict future economic conditions,” Fleming and Kushi wrote. “However, this analysis shows that a growing economy and rising income levels each play a role in increasing the likelihood of homeownership.”

Closing equality gaps

“Not surprisingly, ethnicity and homeownership rates are a frequent topic of research,” wrote Fleming and Kushi, “and often that research identifies homeownership gaps among ethnicities.”

Because all ethnicities cite homeownership as a key component of achieving the American dream, “understanding the observable differences in homeownership rates by ethnicity may help identify ways to advance the prospects for homeownership across all ethnicities,” they wrote.

Controlling for all other factors — educational attainment levels, income levels and other homeownership-related characteristics — narrows the gap, but First American found that all other factors held equal, there were still significant gaps between white homeownership and Asian, black and Hispanic homeownership.

“The real challenge is to better understand why this gap persists,” wrote Fleming and Kushi. “After accounting for all the other factors, are the differences in the homeownership rate by ethnicity due to the challenges of raising a down payment, access to credit, or the impact of more or less financial obligations to extended family members?

“This research can’t answer that question, but it does help to inform the policy discussion about where one might look to further understand why homeownership gaps by ethnicity exist,” they added.